This is a combined analysis of the card payment networks: Visa and Mastercard, basically a global duopoly

None of this is investment advice, this note simply summarizes my research on these companies.

FYI $V & $MA are positions of my stock picking portfolio.

What is the business of Visa & Mastercard ?

Visa and Mastercard are payment infrastructure companies running an open-loop network that connects 4 parties on every card transaction:

Visa and Mastercard are payment infrastructure companies running an open-loop network that connects 4 parties on every card transaction:

- The consumer paying with the card

- The merchant accepting the payment

- The issuing bank (provides the card to the consumer)

- The acquiring bank / PSP (provides the payment solution to the merchant)

They are NOT banks: they don’t lend money, don’t hold deposits, don’t carry credit risk. They simply operate the rails that route the authorization & settlement messages, and take a small fee on each transaction.

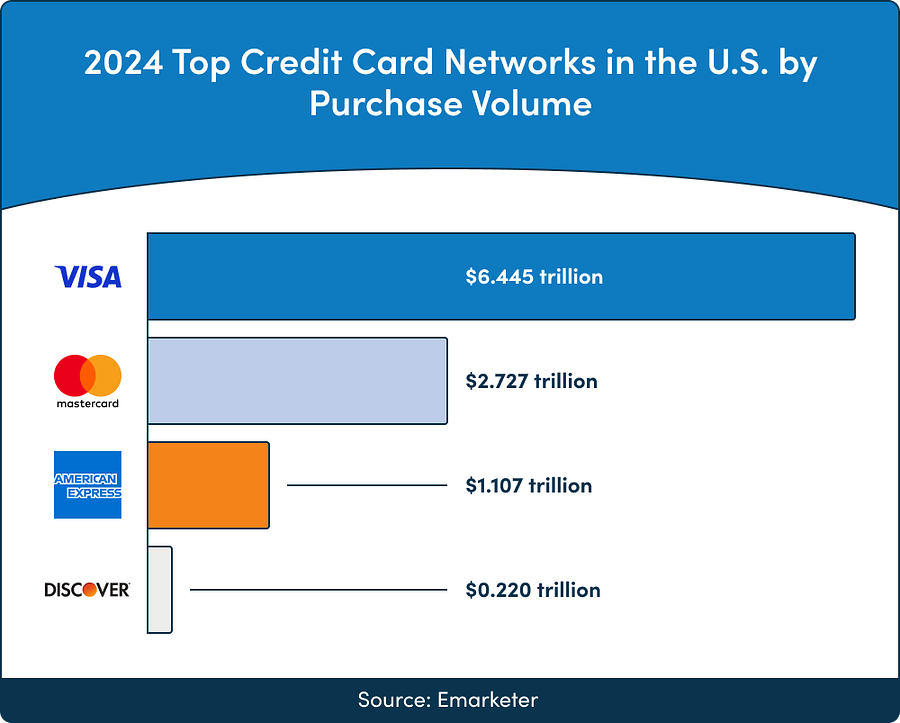

Both have a near-identical business model and dominate their market: in the US they have an estimated 70% / 30% split (2024 purchase volume, Visa being the leader). Worldwide excluding China, Visa alone holds ~50% of card payment volume and Mastercard ~25%, with the rest split across Amex, JCB, RuPay etc.

Both also have insanely high operating margins (their infrastructure is mostly fixed cost, every additional transaction is almost pure profit) and ROCE >35%, making them some of the most profitable businesses in the world per dollar of capital.

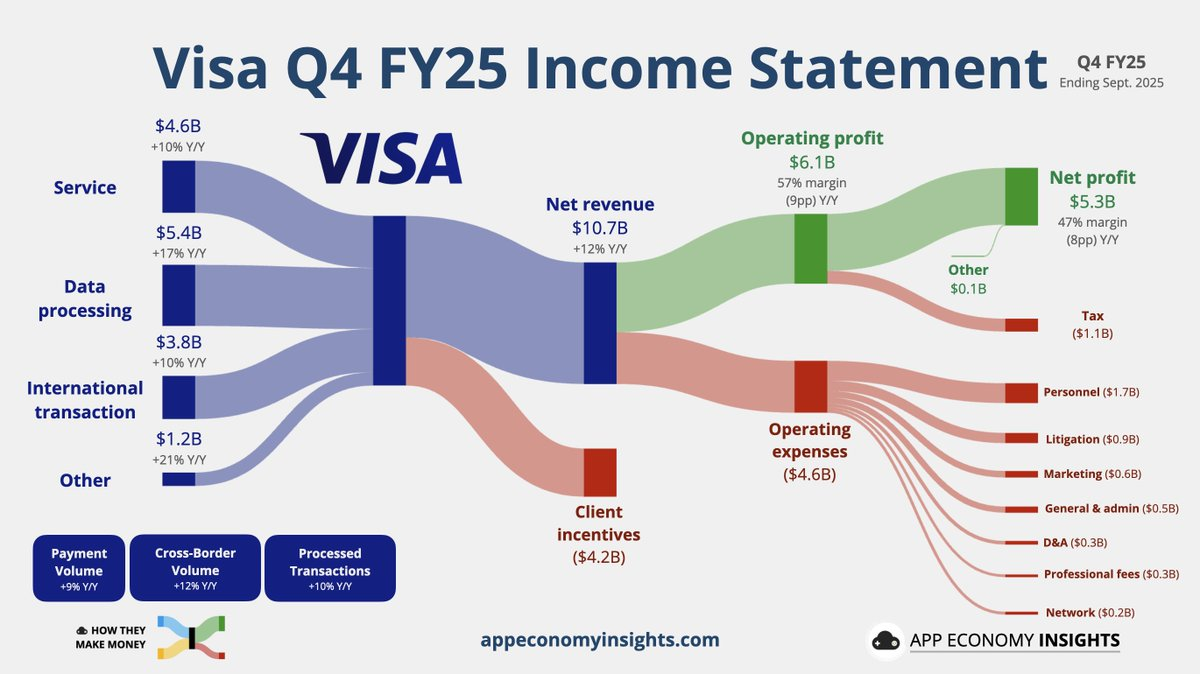

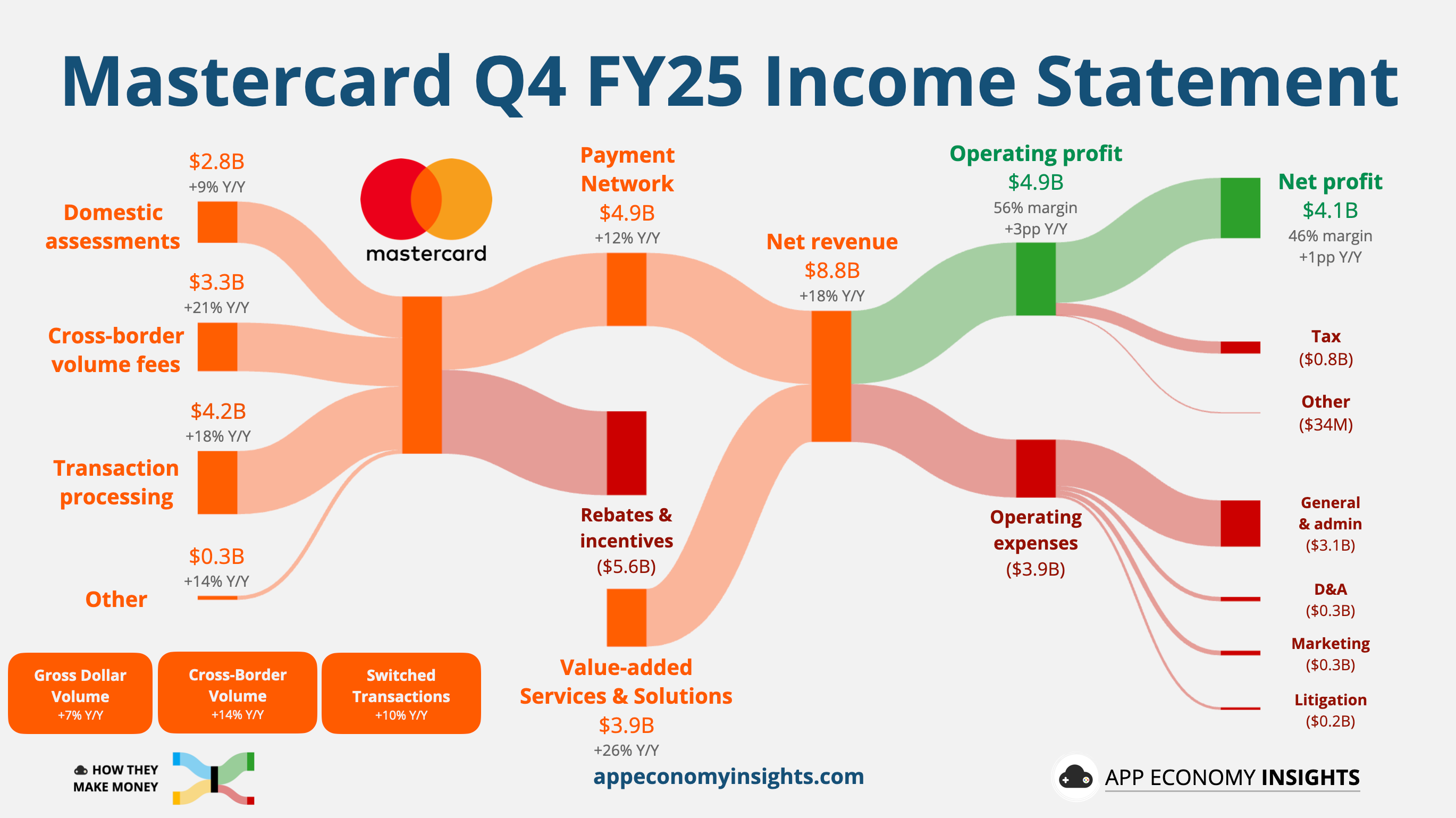

Revenue sources (Visa example, Mastercard is similar)

- Service fees: % of payment volume processed (~0.1% on average)

- Data processing fees: per-transaction fee, not depending on amount (~$0.07/transaction)

- International transaction fees: extra commission on cross-border payments + FX conversion (high margin)

- Value-Added Services (VAS): fraud detection (Featurespace), tokenization, consulting, cloud-based card issuing (Pismo)… fastest growing segment, ~25% of revenue for Visa and ~40% for Mastercard (FY2025)

They also pay back client incentives to issuing banks and merchants to push usage of their network (these are netted out of gross revenue), Mastercard paying more to gain market shares.

Future perspectives & risks

This is the most important part for this duopoly, because the payment industry is being challenged from multiple angles right now.

A2A payments (Account-to-Account)

Bypassing card rails by transferring money directly bank-to-bank, often pushed by central banks & regulators because they are way cheaper for merchants.

Examples of successful A2A networks:

- Pix (Brazil): 160M+ users, default payment method

- UPI (India): one of the largest payment networks in the world by volume, dominates a key growth market

- Blik (Poland): massive adoption

- iDEAL (Netherlands): dominant for e-commerce, now migrating to Wero

In Europe, the Wero / European Payments Initiative (EPI) is the most direct threat:

- 50M+ registered users (Feb 2026)

- E-commerce acceptance live in Germany since late 2025, rolling out in France & Belgium throughout 2026

- POS (in-store) acceptance coming in 2026

- Major merchants signing up: Air France, E.Leclerc, Veepee, Orange…

- Backed by 16+ major European banks → direct attack on Visa/MC’s European business, with the political support of regulators that want payment sovereignty

This is a major structural risk, especially in Europe where there is a clear political will to reduce dependency to US payment networks. But it will probably take time to implement & get adoption, and won’t replace international transactions.

CBDCs (Central Bank Digital Currencies)

Central bank-issued digital currencies could bypass card rails entirely. The biggest current efforts:

- Digital euro: ECB in preparation phase, decision expected in 2026, potential launch 2028+

- Digital yuan (e-CNY): already deployed in China, accelerating (Chinese are using Alipay today and not Visa / Mastercard anyway)

- 130+ countries exploring CBDCs

The threat is real but slow-moving: large-scale CBDC retail payments are years away, and adoption depends heavily on government push (mandates, subsidies). For now more of a long-term watch than an imminent risk. The power of Visa & Mastercard is also in their worldwide acceptance (great when travelling), but the majority of the transactions are happening locally so CBDCs could definitely hurt the transaction volume.

AI Agents with their own payment rails

The risk: in an agentic future, your AI agent does the shopping for you and could route the payment outside of Visa/MC.

However, both networks moved fast and are positioning to capture this:

- Visa Intelligent Commerce (launched 2025): SDK + sandbox, 100+ partners, predicting millions of consumers using AI agents for purchases by 2026 holiday season

- Mastercard Agent Pay: extending network tokenization to AI-driven payments

- Trusted Agent Protocol (Oct 2025): open framework co-built by Visa with 10+ partners

- Stripe integration: supporting both Visa & Mastercard agentic tokens

So far, AI agents are using existing card rails via tokenization rather than building their own. Visa & Mastercard are positioning themselves as the trusted infrastructure for agentic commerce. However, big players (OpenAI, Anthropic, Stripe…) could in theory build their own settlement layer if A2A or stablecoin rails become competitive.

Stablecoins & Crypto

Stablecoin payment volumes hit $33T in 2025 (+72% YoY), with USDC at $18.3T and USDT at $13.3T.

Mostly institutional / cross-border today, but real merchant adoption is starting:

- Shopify merchants processed $800M+ in USDC during 2024 holiday season

- PayPal’s PYUSD, Circle’s USDC pushing into commerce

Both networks chose an embrace strategy rather than denial:

- Visa supports USDC settlement in 30+ countries, $225M+ in stablecoin settlement volume by mid-2025

- Mastercard partnered with MetaMask

- Amex is exploring with Coinbase

But if stablecoins become a default for cross-border commerce, the most lucrative segment (international transaction fees, $14.2B for Visa in FY2025, +12% YoY) is the one most exposed.

I personally have a significant part of my wealth in crypto, so I’m not too concerned about this risk, a global success of stablecoins would make DeFi (Decentralized Finance) & other crypto-native solutions I’m exposed to very successful too.

I also don’t think this is a huge risk, blockchains have their utility for payments but the irreversible transactions & missing fraud detection and other options provided by centralization don’t make them suitable for all kinds of payments.

Big Tech wallets

Today, Apple Pay & Google Pay use Visa/MC under the hood (via tokenization). But if Apple or Google decided to build their own A2A rail (Google already integrates UPI in India, Apple is expanding Apple Cash…), the impact on Visa & Mastercard would be massive.

It currently only abstracts the Visa & Mastercard payment networks, but in makes it easier to replace it with something else with a lower impact on consumer habits.

Regulatory pressure

- US DoJ antitrust lawsuit against Visa on the debit market (ongoing)

- Recurring fines in the EU for “abuse of dominant position”

- Pressure from regulators on interchange fees (already capped in EU)

- Political support for domestic networks (CB in France, Girocard in Germany…)

- Most cards in France are actually doubled stamped with Visa/MC and CB, making the card work on both networks

Growth areas

Despite the risks, there are still real growth drivers:

- B2B payments: massive untapped market ($200T+ globally according to Visa), most still on wires/checks. If cards capture even 1%, volumes could explode

- Cash conversion: still ~$11T paid in cash globally, especially in emerging markets where digitalization is accelerating

- Value-Added Services: fraud detection (AI), tokenization, consulting… estimated TAM of $520B for Visa, of which only ~$8.8B captured in 2024

- E-commerce growth: from $1.2T (2014) to $6.8T (2024), forecasted $10T+ by 2030

- Premium segment (specifically for Amex): pricing power on annual fees still has room

Conclusion

Visa and Mastercard form the most profitable duopoly in the world, with near-impossible-to-replicate network effects, sky-high margins, and disciplined capital return (Visa reduced share count by 56% since 2009, Mastercard similar).

But for the first time in decades, the MOAT is being challenged on multiple fronts simultaneously: A2A payments (especially Wero in Europe, where the political will is strong), stablecoins eating cross-border, CBDCs in the long term (EU again), and uncertainty around AI agents & big tech wallets.

The good news for them is that they are actively moving on these fronts: tokenization, partnerships with stablecoin issuers, AI commerce SDKs… they have the cash and the network position to adapt. But it’s the first time we can imagine a credible scenario where their dominance is meaningfully eroded.

I have about 15% of my stock-picking portfolio in $V & $MA currently, but the valuations are often too high given the disruption risks I see.\

They are still exceptional businesses but I’m looking into diversifying in the payment sector with V given the current valuations) to rebalance my portfolio with it.