This is an analysis of Alphabet ($GOOGL), exploring their business and diverse sources of revenue.

None of this is investment advice, this note simply summarizes my research on this company.

FYI $GOOGL is one the biggest positions of my stock picking portfolio

What is the business of Alphabet ?

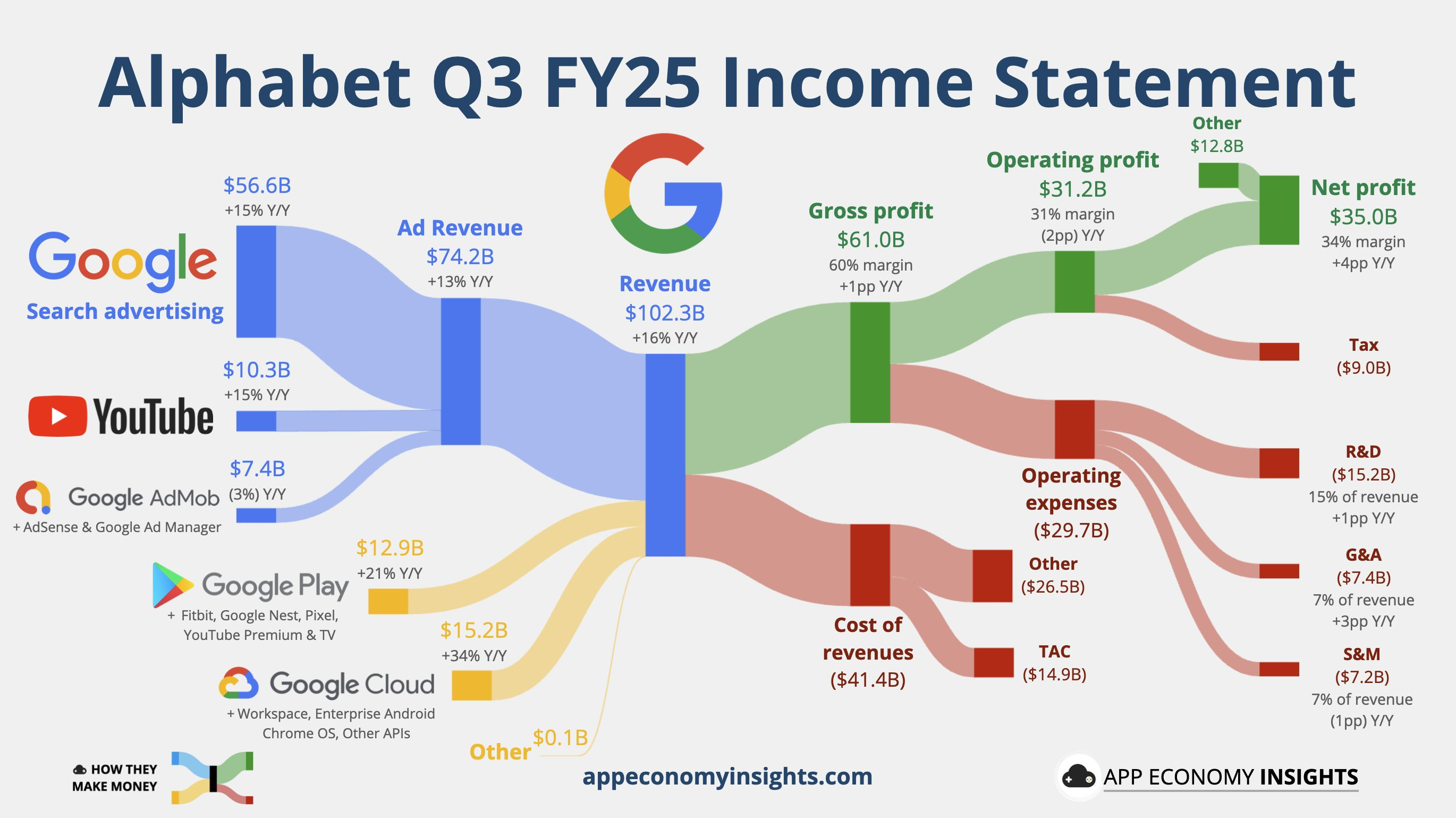

Alphabet is an information and data company that makes the vast majority of its money through digital advertising. It’s currently the most profitable company in the world.

It has 3 main pillars:

- The Ad Machine: Heart of the business, ~75% of total revenue

- Google Search (payments from companies to appear at the top)

- YouTube (ads watched before watching videos)

- Display Network / AdSense (middleman placing ads on millions of non-Google websites and taking a cut of the fee)

- Computing Infrastructure: Google Cloud, fastest growing segment

- Provides compute power, AI services & technical infrastructure

- Hardware & Subscriptions

- Pixel phones, Nest smart home devices, Fitbit wearables for hardware

- Google Play (cut from app sales), YouTube premium, Google One storage, Google workspace for subscriptions

This is a general summary of Alphabet’s activities, as it’s a tentacular company with a lot of other components described below as extensively as possible.

Detailed services description

List of all the services / companies part of Alphabet.

See also this list (in French).

Consumer services

- Google Search (90% market share (4% Bing, 1.5% Yandex, 1.26% Yahoo, 0.78% DuckDuckGo)

- Google Maps (80% market share) / Google Earth

- Google Workspace (Drive, Calendar, GMail, Photos, Meet, docs / sheets…)

- Google News (news aggregator)

- Google Scholar (scientific publication search engine)

- Google Pay

- Google Translate

- Chrome (71% market share), ChromeOS

- YouTube (more hours watched than Netflix, YouTube music 8% market share)

- Waze

- Gemini (with DeepMind)

Consumer hardware products

- Nest (smart devices)

- Fitbit

- Android (securing app store revenue / default apps installation)

- Pixel (phones, tablet, headphones, watches)

- Chromebook (hardware by 3rd party companies but using ChromeOS)

Developers & IT infrastructure

- Google Cloud

- Includes AI services with Vertex AI / Gemini

- Google Maps API (60% market share)

- Used by Uber, Domino’s Pizza, 7/11 Japan…

Enterprise solutions

- AdSense

- Google Workspace

Others

- Waymo (autonomous driving)

- Verily (study of life sciences)

- Calico (human health / overcoming aging)

- Sidewalk Labs (urban planning)

- Wing (drone delivery)

- Isomorphic Labs (AI-powered drug discovery)

- GFiber (internet access)

- Google X (innovation lab for experimental projects)

- CapitalG (private equity)

- Invested in AirBnB, Stripe, Duolingo, Lovable, Robinhood, Kalshi…

- GV (Google Ventures, VC)

- Invested in Vercel, GitLab, Nothing, Uber, Slack…

- SpaceX (7% stake), rumored to IPO in 2026 at a $1.5T valuation → $111B

- Anthropic (~8% stake)

Future perspectives & risks

Artificial Intelligence

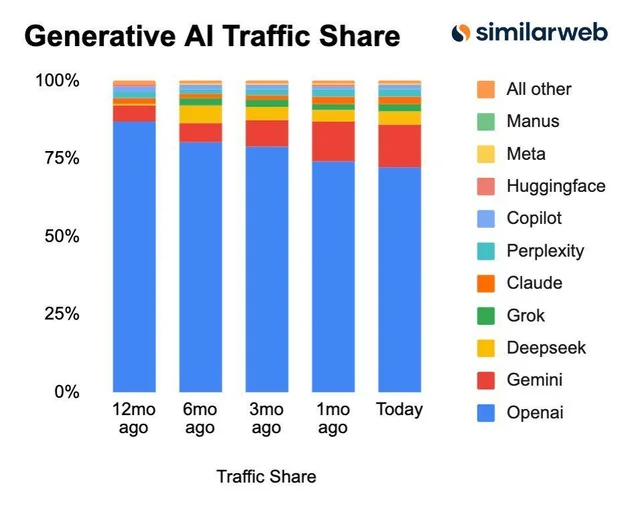

AI might disrupt Google Search & its related Ad business, but:

- Google is well positioned in the current AI race, gaining market shares against OpenAI / ChatGPT. They also have tremendous cashflow that they can inject to keep pushing, vs OpenAI bleeding money everyday.

- Google Search revenue is still growing double digits since 2022 (release of ChatGPT), so I’m not personally convinced that AI search will completely destroy Search (especially once the actual inference & LLM training costs will be reflected on users that currently have huge free tiers due to the AI race competition).

- Google is the only one with a complete AI Stack in-house with their TPUs (which are overhyped currently imo but still an important thing to consider)

- While text model leaders frequently rotate on lmarena, DeepMind is very frequently leading in image (generation / vision) and video

- Integration of AI features in their products will allow them to increase prices (Workspace) and offer new services (Vertex AI, AI Studio, Flow…)

The market of consumer AI / AI search is still very fresh and fragile, there is ChatGPT vs Gemini (and Grok / Claude etc) but also Chinese companies (DeepSeek, Qwen, Kimi, Z.AI, Hunyuan…) taking the open-source approach, and we don’t know where this will lead.

For example, SLM (Small Language Models) also can’t be discarded completely, maybe in the future we will have a chat with an SLM running locally on our phone / computer instead of using an app like ChatGPT?

Anyway imo its a win-win for Google, if AI search doesn’t take over they still have their Search monopoly, if it does they are well positioned to be a (if not THE) leader of consumer AI (and probably also of enterprise AI).

Regulations & market dominance

Alphabet has always been under intense regulatory scrutiny due to its huge monopolies, but can this be a risk in the future?

I don’t really think so as:

- Google won’t be forced to sold Chrome according to a recent ruling, and the only competitor of Chrome / Chromium is Firefox from Mozilla, which is making 80% of its revenue from Google (to make it the default search engine). The power of Chrome (and Android) is making Google services the default, and today also bring AI experiences powered by Google to the masses (to compete against ChatGPT Atlas or Perplexity Comet)

- Alphabet benefits from the interconnexion of its services (DeepMind Gemini embedded in Workspace & offered in Google Cloud, AdSense for Search, Maps etc…), but in case of a forced dismantling shareholders would received shares of all the underlying companies anyway, and while I’m not hoping for it if it were to happen I’m pretty sure the combined market cap of the resulting companies would be higher as most people don’t realize the scale and diversity that Alphabet offers. I’m in line with what is said in this post (in French) about potential dismantling value.

Growth areas

Business segments where I see growth potential:

- Google Cloud: 3rd largest provider (behind AWS and Azure) but bigger growth rate (especially compared to AWS), which can accelerate a lot with Gemini & related AI services

- DeepMind (Gemini, Nano banana, Veo…) with all the AI services they offer

- Waymo for autonomous driving. This is a complex topic with questions like Waymo vs Tesla (the 2 major players today), the place of Uber (will it thrive more with this revolution or disappear) that I haven’t explored in depth yet, I agree with this analysis (in French) and its conclusion:

For Alphabet, the Waymo bet represents a positive asymmetry. If it succeeds—and the initial figures are encouraging—it could generate hundreds of billions of dollars in growth.

The key point? The market hasn’t yet priced this in. If Waymo fails, Alphabet remains a profitable giant. Conversely, if Waymo succeeds, it’s a real jackpot.

For Tesla, it’s a different story. The market already values the company as if autonomous driving is a given thing. If Tesla succeeds, which remains likely given its massive database, the valuation can be justified, and the story continues.

If Tesla fails or falls behind, there’s no safety net. The disappointment would be brutal, because electric car sales alone aren’t enough to justify the market capitalization.

- Potentially a lot of the companies of the “Other Bets” category that I’ve mentioned above (or just completely forgot, which is very probable too), Waymo is the most popular one today but others might emerge

- Other segments that are already huge today might grow

- YouTube taking a bigger share of:

- live streaming against Twitch / Kick

- music (not very convinced about that but might happen)

- film / series to compete against Netflix & others

- Google Workspace taking a bigger share of the enterprise market (not convinced about that too, but I personally find Google Workspace to be way better than Microsoft 365)

- Android (and thus Google Play / Google apps) taking a bigger share of the smartphone market against Apple, again not very convinced (I’m personally an iPhone user and not planning to change) but as Apple is lagging behind in AI it might happen (there are also talks of custom Gemini integrations for Siri, so a win-win situation for Google again).

- Google Pay: While Mastercard are great stocks, they will face risks in the future (A2A payments, stablecoins, regulations…) that might disrupt them, while Google Pay (and Apple Pay for iPhone) is probably here to stay and can easily adapt, like they are doing in India where they integrated UPI. It’s not a huge revenue opportunity, but still a nice add-on

- YouTube taking a bigger share of:

Conclusion

Alphabet is a tentacular company positioned in A LOT of segments, many of which they are the uncontested leader.

Despite its revenue dependence to Search, the diversification is incredible and growing year over year.

I also like that there is no single public figure holding the whole company like Elon Musk for Tesla or Jensen Huang for Nvidia (there is Larry Page & some huge talents at DeepMind, but this is not the same scale), which I’m not very comfortable with to predict what would happen when they leave.

It’s the most profitable company in the world today and I don’t see a world where they don’t stay at the top (or at least in the podium). It’s currently the 3rd company by market cap, only after:

- Nvidia, which is in the semiconductor space that I find very complicated to fully correctly understand, has a very prominent CEO which is not something I’m found of & a high dependence to the current AI race. Its a great company (that has a correct valuation imo at the time of writing) but for these reasons I didn’t analyzed it in depth, exposure to it with ETFs is enough for me.

- Apple, which isn’t growing as fast as it used to be and without visible signs of improvements. Still generating huge revenues, but not a stock I would like to own individually.

This is why $GOOGL is currently the biggest position of my stock picking portfolio.