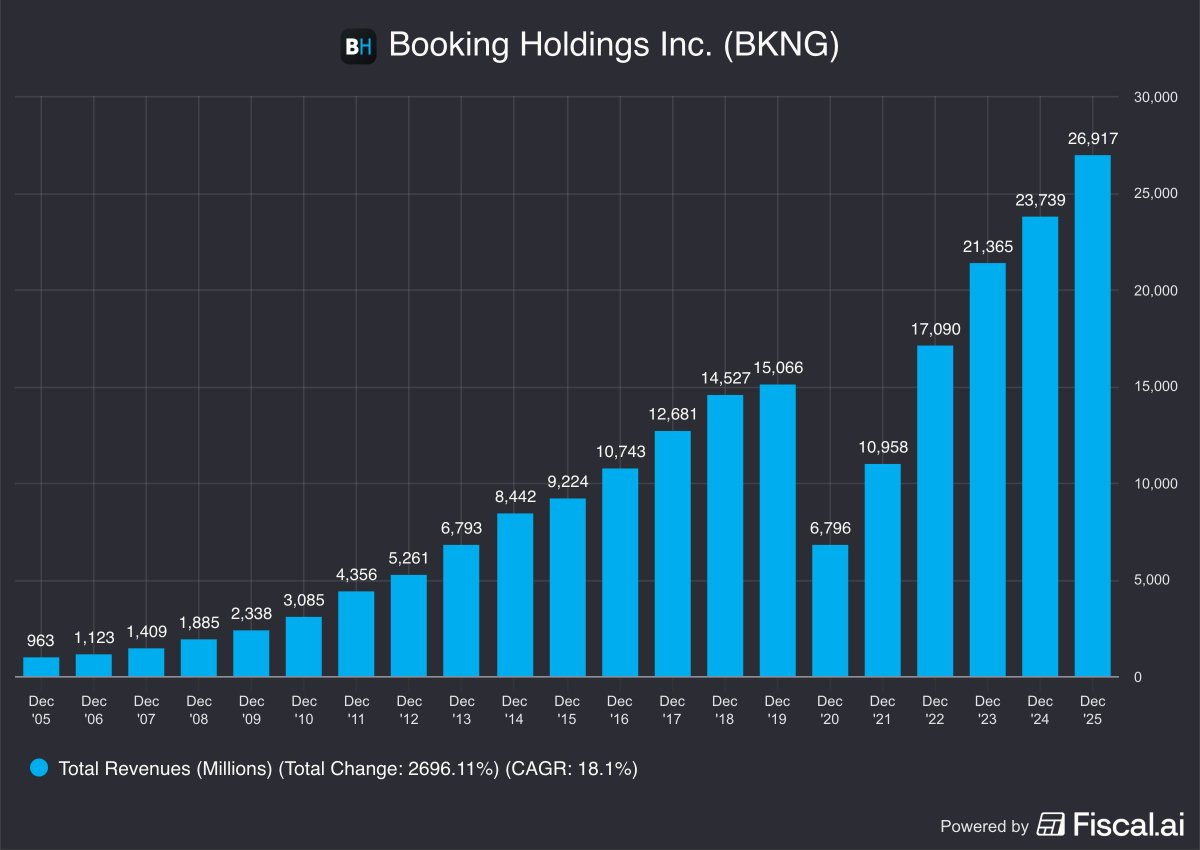

This is an analysis of Booking Holding ($BKNG), exploring their business and diverse sources of revenue.

None of this is investment advice, this note simply summarizes my research on this company.

FYI $BKNG is one of the positions of my stock picking portfolio

What is the business of Booking ?

Booking Holding is one of the key players in the global travel market, with brands like Booking.com, Kayak, Priceline, Agoda…

It’s the biggest OTA (Online Travel Agency) operating in several categories:

- Accommodations (both hotels & personal homes like AirBnB), the biggest source of revenues with 2 models (Merchant and Agency)

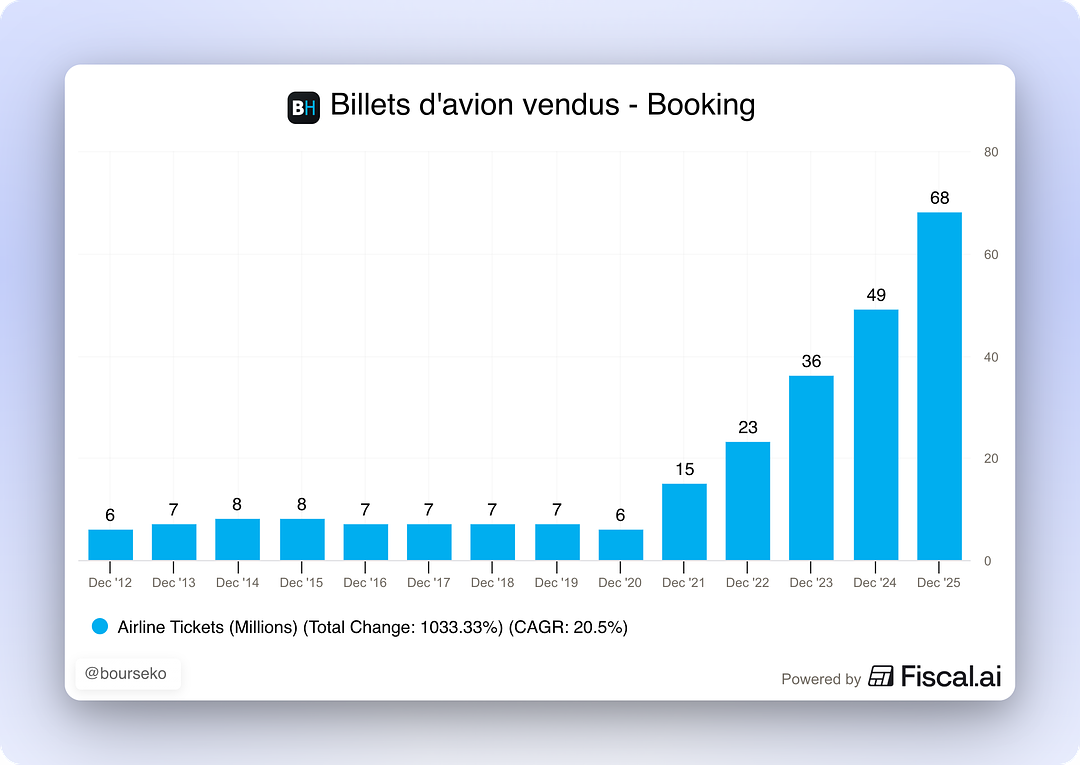

- Flights, a growth opportunity & important segment to keep the users in the ecosystem

- Car rentals with Rentalcars.com

- Experiences & attractions

- Restaurants with OpenTable

Detailed services description

List

List of all the services / companies part of Booking Holding.

- Booking.com (the main platform with hotels, flights and experiences)

- Also a lot of personal homes, they are growing faster than AirBnB and have currently about 80% of AirBnB’s total nights on that segment alone

- Kayak (meta research, with ads as the main revenue)

- Priceline (historical brand, mostly present in North America)

- Agoda (the Asian Booking.com)

- Rentalcars.com (asset-light car rental)

- Traditional rental companies (Hertz, Sixt, Avis…) are asset-heavy (1000s of vehicles, maintenance…)

- Like the rest of the group, Rentalcars doesn’t own anything, it’s simply the aggregator

- OpenTable.com (restaurants booking)

Sources of profits

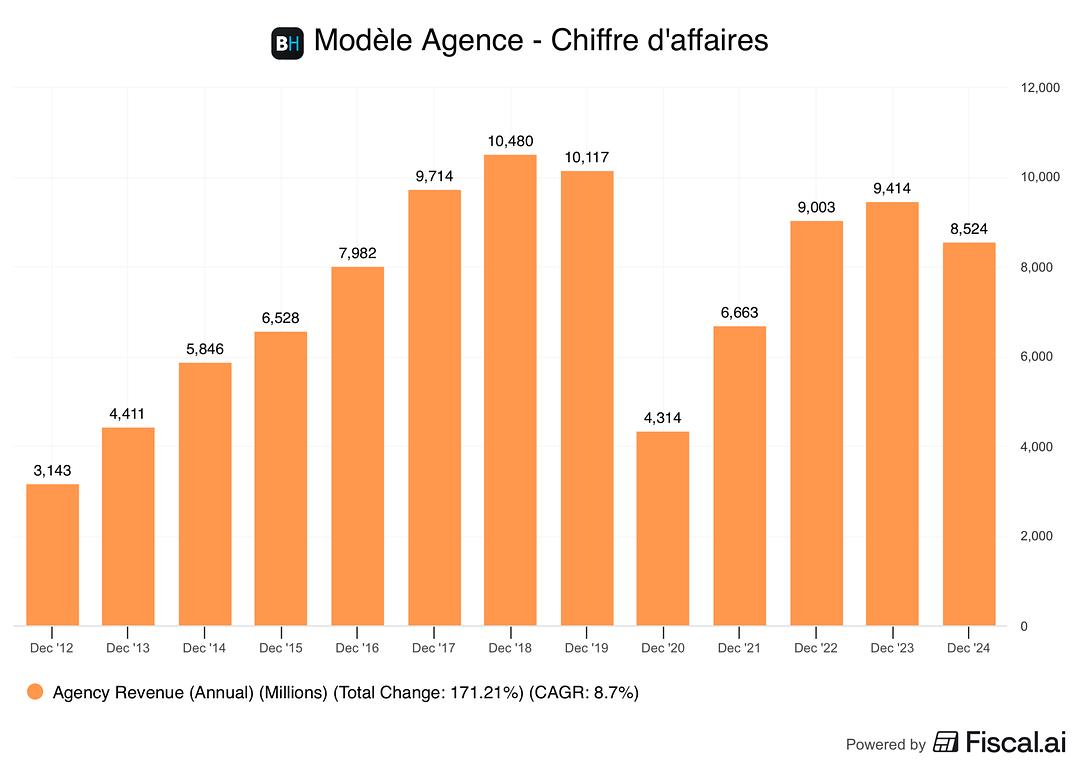

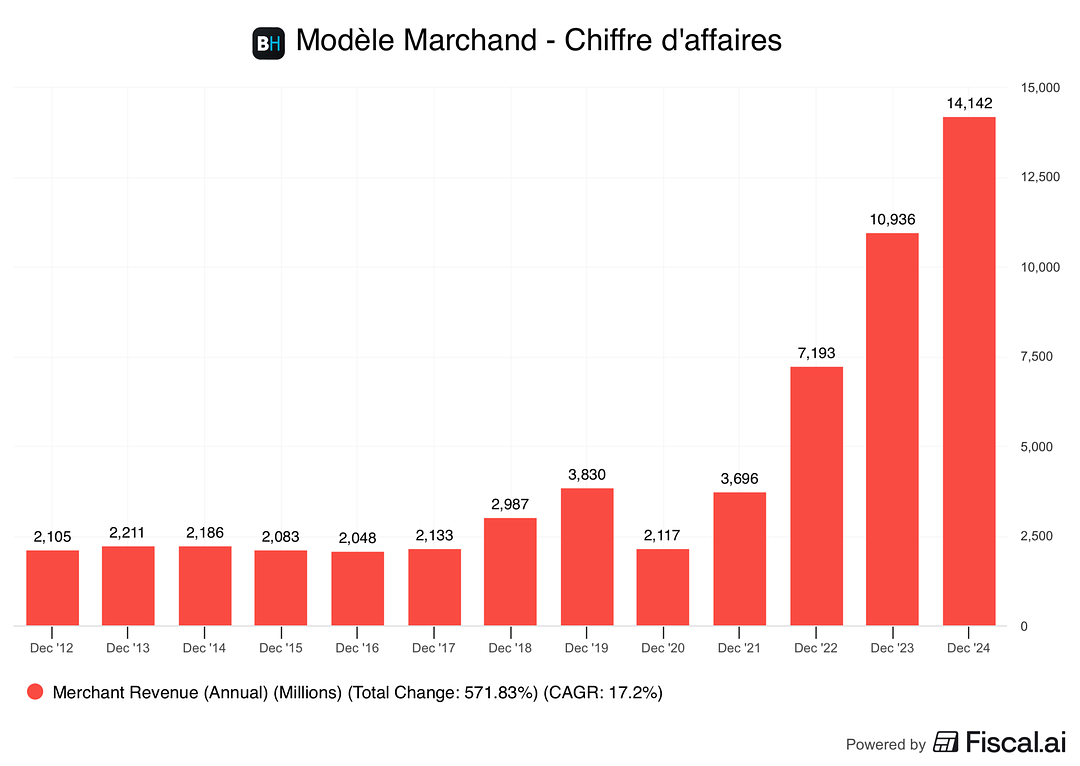

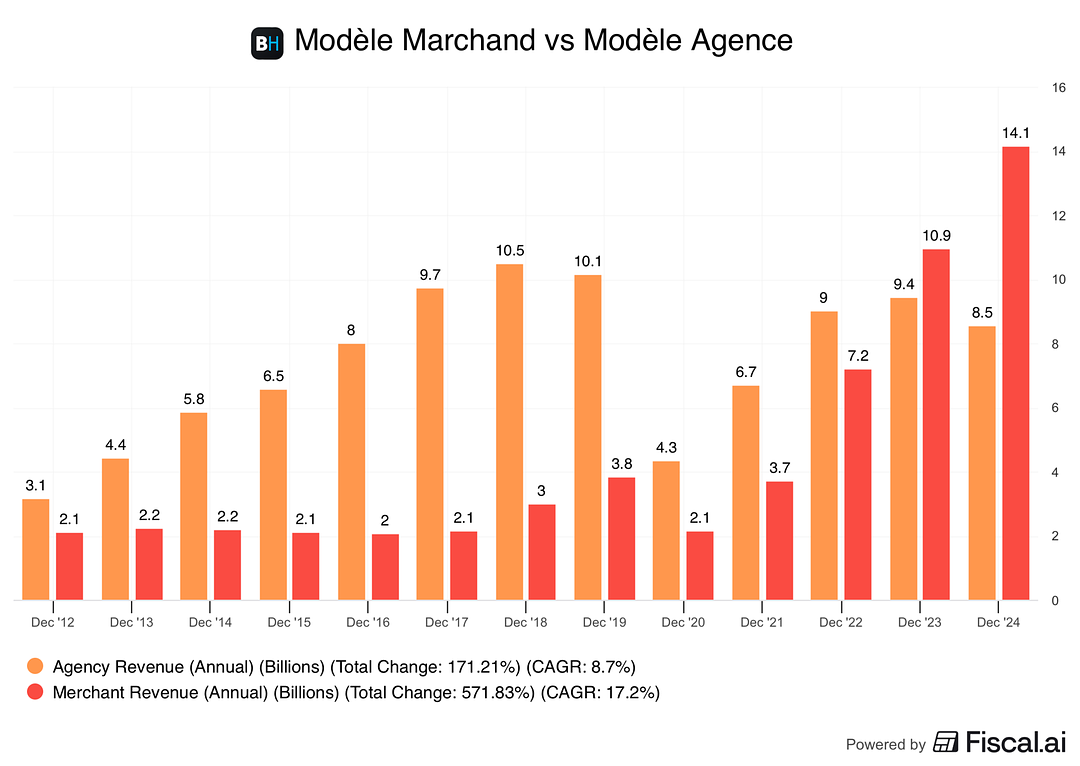

Booking.com operates with 2 models.

The historical one is the agency one, where Booking is simply the business introducer (🇫🇷 apporteur d’affaires), the client books on the platform but pays the hotel directly when he arrives, and Booking collects its commission from the hotel at the end of the month.

The second model, merchant, is the most interesting and the one Booking is pushing.

Here, Booking becomes the official merchant and processes the payment, then sends to the hotel its part (total price minus their commission).

The advantage is total: they secure their commission right away and have a float (excess treasury between the moment the client pays and when they pay the hotel), basically a 0% interest credit.

This is also reducing friction for the consumers & the different means of payment (Indian customers can pay with UPI or Chinese one with AliPay and the hotel in France can be paid in euros) and allows Booking to push the “Connected Trip” (sell the whole trip with flights, attractions etc, bringing revenue with no acquisition cost to the other segments).

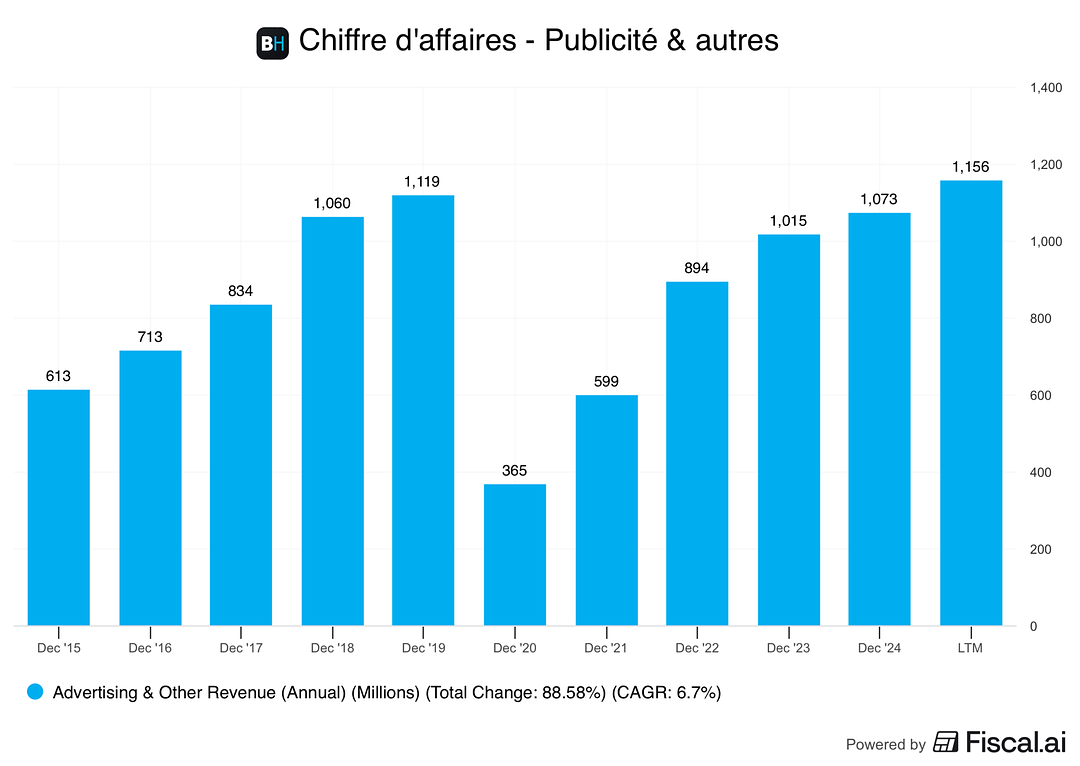

Booking.com remains the major source of revenue, but some other segments are increasing such as Ads (on Kayak, on Booking for hotels to increase their visibility…), OpenTable fees… it’s a small segment but worth mentioning with its low cost of operations.

Future perspectives & risks

Artificial Intelligence

This is the biggest risk that is being priced by the market right now, pretty much like all software stocks.

But in my opinion, Booking.com won’t be disrupted by AI, it will leverage it to be grow even stronger.

The fear is basically that clients will stop using Booking and instead just use ChatGPT or other AI assistants to plan their trip and book it (or in an agentic future, our personal agents will plan it, submit it to us for approval and then handle the booking). But:

- These integrations are built with Booking.com today, and they are also creating their own in-house AI trip planner.

- This is a vast and complex business, Booking is the payments & settlements in various currencies, the relationships with hotels, many of which are small independent ones, the customer service when there is an issue, handling the local norms and laws… it’s not just a business where an AI company (or any vibe coder) can come and create a serious competitor, because the MOAT here are the network effects (more hotels give more choice to consumers, which are more inclined to browse the catalog), the cost advantage (they are spending a lot in marketing and ads so it will be hard for a competitor to carve its piece of the cake), the brand (and the serenity that goes with it, knowing that Booking is here acting as a trusted intermediary)…

- They have everything they need to build this themselves: the accommodations base, the flights booking, the experiences & attractions, car rentals, airport taxis… if somebody can build this “Connected Trip” (more on that below) it’s them, and the management is great & will leverage this opportunity imo

Macroeconomy & consumption habits

The travel sector obviously depends on the will (and capacity) of consumers to travel, an economic contraction / crisis can impact the demand.

Geopolitical instabilities can also reduce travel to affected countries / regions, sometimes durably.

Regulations & hotels relationship

Laws and regulations can impact the business of Booking, like the Digital Markets Act which now allows hotels to propose prices lower that what is on Booking.com on their own sites, or other antitrust decisions.

The second ones is the hotels, that are structurally dependent on Booking.com but are also trying to get rid of it (for example when a customer books a stay, when he arrives they will try to register him to their loyalty program so next time he books directly with them). I’ve even had an experience myself in Malaysia where the hotel cancelled the Booking reservation in front of me and made me pay directly to them a lower price for a better room 😅 (but this is an extreme case where the hotel is playing with fire).

But again, Booking is still irreplaceable today, and hotels will prefer filling a room for fee than keeping it empty.

Growth areas

The focus on the Agency model and the potential switch of the Merchant one towards it is an important factor to consider as the Merchant model is still representing a big chunk of the revenue.

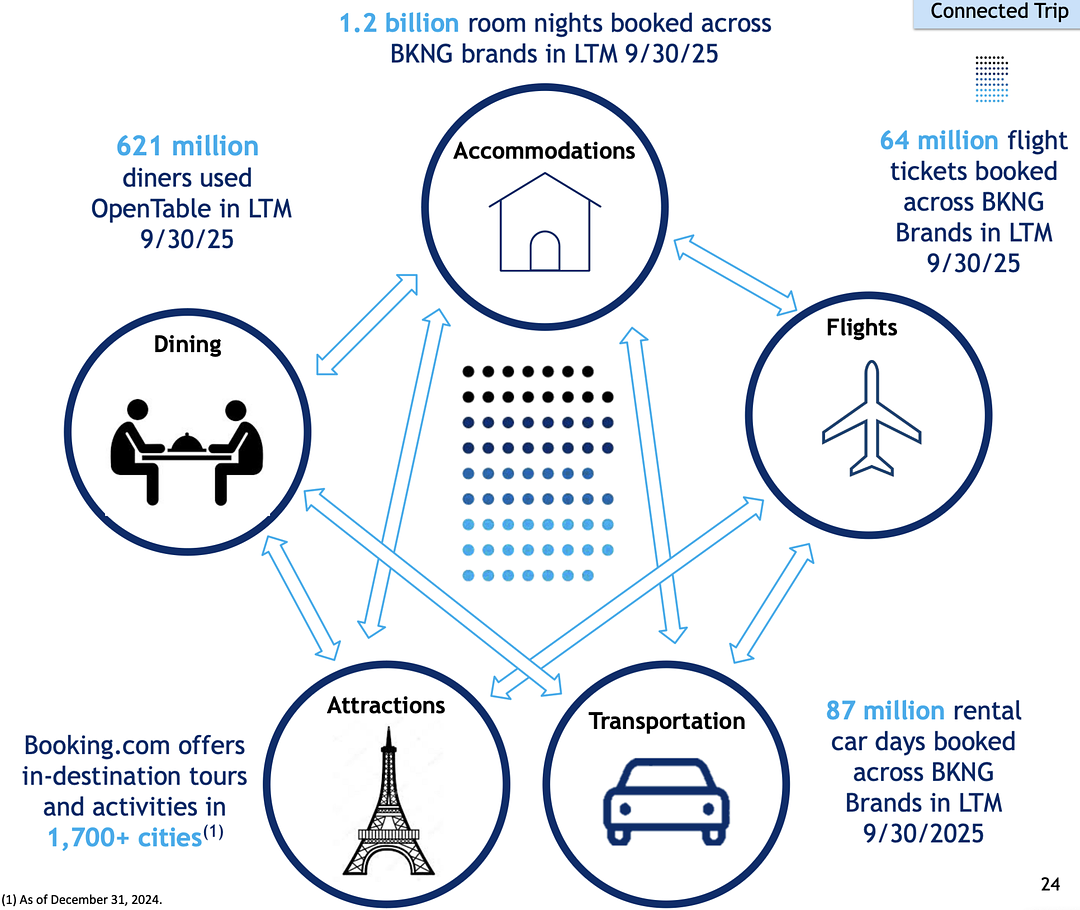

The Connected Trip vision also has the potential to be a huge growth driver, as I mentioned earlier I think if anybody can pull it off its Booking.

It can become a real travel ecosystem to fully plan and book your trips, and the management has a great execution and vision on this, with this interview of the CEO being particularly interesting.

The step after the Connected Trip is even bolder, it’s having a self-healing trip: if Booking is handling everything, with AI they could handle all the changes in the case of a cancelled flight for example (propose an alternative flight, adjust the time of the airport taxi transfer, notify the hotel…).

Booking also has a lot of frequent travelers, with 55% of their volume in 2025 coming from Genius 2 & 3 members (their loyalty program), a user base that can definitely still grow and be leveraged in the Connected Trip vision.

Finally, also linked to the Connected Trip and the revenue it can bring to the whole ecosystem but Booking is expanding in all the verticals of travel, like flights for example, which have lower margins that accommodations but are still driving revenue up.

Conclusion

Booking.com is the biggest Online Travel Agency, present in all the segments from accommodations to flights, car rental, attractions or restaurants reservations.

It has a very competent management with a great vision on the future of travel (Connected Trip, self-healing trip…) that can bring significant growth to a business that already generates a lot of cash.

While it has some risks, the biggest one currently priced by the market is the AI disruption one, and I think that it’s actually the opposite where Booking will actually increase its market share and create the one-stop shop for travel all over the world.

This is why $BKNG is currently one of the positions of my stock picking portfolio.